CSS Accountancy and Auditing Syllabus

PAPER: ACCOUNTANCY & AUDITING (200 MARKS)

Paper-I (MARKS-100)

(A) Financial Accounting (50 Marks)

I. Fundamental Accounting Principles, Concepts, Assumptions and Conventions:

Nature and Scope of Accounting, Accrual/Matching Concept, Consistency of Presentation and Comparability, True and Fair View, Neutrality, Materiality, Prudence, Completeness, Understandability and Usefulness, Going Concern, and Substance over Form.

II. Accounting Cycle/Process and Financial Statements:

Transactions and/or Events, General Journal, General Ledger, Trial Balance (Unadjusted),Adjusting Entries and Adjusted Trial Balance, Work Sheet, Financial Statements including Income Statement, Statement of Financial Position (Balance Sheet), Statement of Cash Flows and Statement of Changes in Equity in accordance with the Financial Reporting Framework as specified by International Accounting Standard Board (IASB) through IFRSs/IASs, and by Securities and Exchange Commission of Pakistan through Companies Ordinance 1984, and Closing and Reversing Entries

III. Attributes, and Significance of Accounting Information:

Attributes of Accounting Information, Information/Reporting Requirements of various Users/Stakeholders of Financial Statements including External (Investors/Shareholders, Creditors, Suppliers, Lenders/Financiers, Government Agencies etc.) and Internal (Board of Directors, Partners, Managers, Employees etc.) Stakeholders.

IV. Accounting for common Legal Forms of a Business:

Accounting Principles and Financial Statements of Sole-proprietorships, Partnerships and Joint Stock Companies including Banking Companies (Excluding Advanced Topics like Amalgamation, Capital Reduction, Consolidation etc.)

V. Accounting for Associations Not-for-profit, and for Public Sector:

Accounting Principles and Financial Statements – of Associations Not-for-profit, and – of Public Sector Entities as per Standardized Financial Reporting Framework provided by International Public Sector Accounting Standards (IPSAS) Board and Practices being followed in the country.

VI. Accounting for Non-current Tangible Assets:

Fundamental Concepts and Principles concerning Non-current Assets: Cost; Depreciable Amount; Depreciation; Fair Value; Property, Plant and Equipment; Residual Value; and Useful Life. Depreciation Methods and their Application (as specified by International Accounting Standards Board):Straight-line Method; Reducing Balance Method; Number of Units Produced and basic know-how of other Methods/Techniques being commonly used by the Industry.

VII. Fundamental and Technical Analysis of various Forms of Organizations:

Financial Statements’ Analysis including both Horizontal (Measuring Change) and Vertical (Ratio) Analysis including Liquidity Ratios, Activity Ratios, Debt Ratios, Profitability Ratios and Market Ratios; Technical and Industry Analysis.

(B) Cost and Managerial Accounting (50 Marks)

VIII. Fundamental Cost Accounting Principles and Concepts:

Nature and Scope of Cost and Managerial Accounting; Cost Concepts, Elements and Classification; Underlying Differences among Financial, Cost, and Management Accounting.

Accounting for Material, Labour and Factory Overheads (FOH):

Recognition and Valuation Principles for Material Inventory, and Methods to control Material Inventory; Calculation/Measurement and Accounting for Payroll for all forms of Labour, Time Rate and Piece Rate Systems; Commonly used Group Incentive Schemes; Factory Overhead Costs and FOH Rate, Departmentalization of FOH Costs, their Allocation, Apportionment and Reapportionment (Primary and Secondary Distributions), Methods for Secondary Distribution including both Repeated Apportionment/Distribution and Algebraic Method.

Costing for Specific Jobs, and Process Costing:

Nature of a Specific Job, and Job-order Costing; Process Flow and Process Costing by the use of Cost of Production Report (CPR).

Management Accounting for Planning, Decision-making and Control: Budgeting and its Use:

Meaning and Nature of a Budget; Major Forms of a Budget including Production and Sales Budget, Cash Budget, Flexible Budgets, Zero-based Budget, Master Budget etc.

Break-even Analysis:

Difference between Marginal and Absorption Costing Techniques; Concept of Relevant Cost; Application and Use of Contribution Margin and other Concepts for Planning and Decision-making (under Break-even Analysis)

Variance Analysis:

Meaning and Use of Standards and Variances; Major Classification of Variances including Material, Labour and FOH Variances, and their Computation.

Paper-II (MARKS-100)

(A) Auditing (40 Marks)

Fundamental Auditing Principles and Concepts:

Audit and Auditing, True and Fair View, Audit Assertions, Reasonable Assurance, Documentation and Audit Evidence, Audit Program, Audit Risks, Computer Information Systems (EDP Systems) and Computer-assisted Audit Techniques (CAAT), Inspection, Fraud, Going Concern, Audit Materiality, Misstatement, Governance and Premise, Tests of Control and Substantive Procedures.

Audit Considerations, Dimensions and Conduct:

Internal Control System and Internal Audit, Internal VS External Audit, Responsibility for Financial Statements, Audit Planning, Scope of an Audit, Objectives of an Audit, Inherent Limitations of an Audit, Risk Assessment and Management, Internal Audit and Corporate Governance, Classification of Audit, Qualities of an Auditor, Auditing in Computer Information Systems (EDP Systems) and Computer-assisted Audit Techniques, General Auditing Principles and Techniques commonly applicable to various Types of Undertakings including Merchandizing, Manufacturing, Banking, Insurance, Investment Entities etc., Audit Performance and Audit Completion.

Role and Responsibilities of an Auditor:

Auditor’s professional and legal Rights, Responsibilities & Duties, and Liabilities; Auditor’s Opinion and Report, and their classification (Types); – as specified under the Companies Ordinance 1984, and in the handbook of IFAC.

(B) Business Taxation (30 Marks)

1.Tax Structure, and Fundamental Concepts vis-à-vis Income Tax in Pakistan:

Tax Structure in Pakistan; Fundamental Definitions/Terminologies defined under Section 2 of the Income Tax Ordinance 2001.

2.Income Tax and Sales Tax Principles, and their Application:

Selected Provisions from Income Tax – Income for Tax Purposes [Section 4, 9 & 10], Heads of Income [Section 11], Tax Payable on Taxable Income [First Schedule to the Ordinance], Salary Income and Taxation [Sections 12 to 14], Income from Property [Sections 15 & 16], Income from Business[Sections 18 to 20], Capital Gains[Sections 37 to38], Income from other sources[Section 39, 40, 101(6), 111],Tax Credits [Sections 61 to 65], Taxation of Individuals, AOPs and Companies [Sections 86, 92, 94], Due Date for Payment of Tax [Section 137], Deduction of Tax at Source/With-holding Tax [Sections 147, 149, 153, 155]and related Income Tax Rules 2002. Selected Definitions and Provisions from Sales Tax –Scope of Tax [Section 3], Exempt supply [Section 2(11)], Goods [Section 2(12)], Input Tax [2(14)], Registered person [Section 2(25)], Supply [Section 2(33)], Tax [Section 2(34)], Retail Price and Retailer [Section 2(27)& 2(28)], Taxable Activity [Section 2(35)], Taxable Supply [Section 2(41)], Tax Fraction [Section 2(36)], Tax Period [Section 2(43)], Time of Supply [Section 2(44)], and Determination of Tax Liability [Section 7].

(C) Business Studies, and Finance (30 Marks)

Business Studies:

Nature and Scope of a Business Entity, Contemporary Challenges posed to a Business; Common Legal Forms of a Business Entity – Sole proprietorship, Partnership, Joint Stock Company, their Features, Formation and Management; Business Combinations and their Scope; Business Cycle and its Implications; Role of Information Technology in Business.

Finance:

Meaning, Nature and Scope of Finance, and Financial Management; Common Modes (Types) of Business Finance – Short-, Medium-, and Long-term Financing; Nature and Scope of Financial Markets and Institutions; Features and Classification of Financial Markets; Financial Management Techniques for Decision making: Time Value of Money, Cost of Capital and Capital Budgeting Techniques.

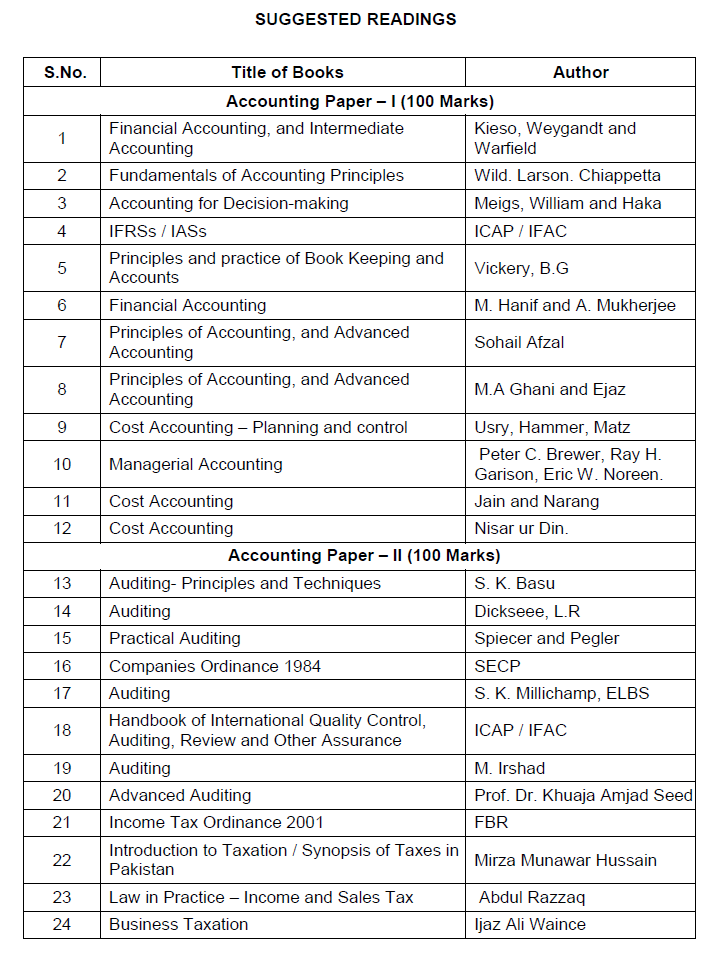

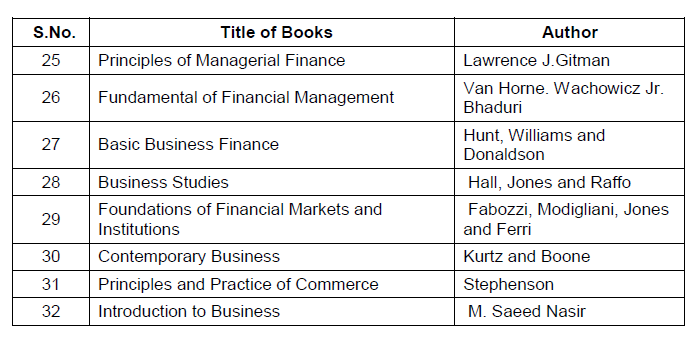

Suggested/Recommended Readings:

Download CSS Accountancy and Auditing Past Papers

Download CSS Accountancy and Auditing Books

Download Full CSS Syllabus

CSS Accountancy and Auditing Syllabus